Just prior to Halloween, the UN announced that levels of CO2 in the atmosphere reached new record levels of 403 ppm in 2016. The shipping industry remains a broadly efficient transportation solution in terms of emissions per tonne of cargo, but the news will only increase the focus on what new action may now be necessary, against the spectre of substantial fleet growth over the last decade.

Scary Stuff?

Unlike in the case of emissions of NOx and SOx, CO2 emissions have so far not seen ‘top-down’ efforts lead to a deadline such as the 2020 global sulphur cap. However, the EEDI system was implemented in 2013, and the EU will introduce a monitoring regime for ships calling at EU ports from start 2018. However, in addition to ‘top-down’ EEDI regulations, owners’ actions have also begun to have an impact. Whilst stimulated initially by a desire to save on bunker costs, moves into “eco” ships (and towards slower speeds) have also helped to limit emissions.

Trick Or Treat?

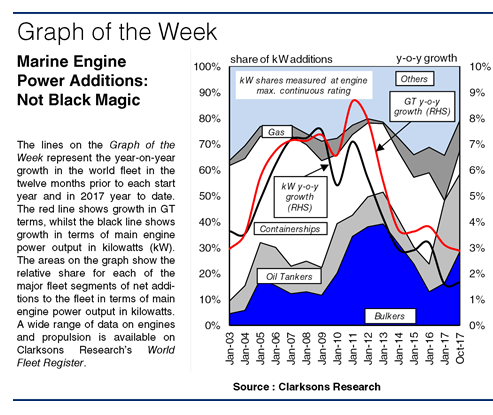

During 2003-08, the fleet grew by 34% in GT, and 32% in kW main engine power terms. More than 40% of net growth in kW terms was represented by containerships. But, following the onset of the downturn, slow steaming and a focus on “eco” ships meant that a gap appeared between the growth rates in GT and kW. In 2008-13, despite 42% growth in GT terms, the fleet grew by 34% in kW. In fact, annual growth of the world fleet in kW terms was 2.2 percentage points slower than growth in GT terms by 2012. Although slightly narrowed, a differential has been preserved in subsequent years.

Deliveries of containerships optimised for slower steaming were a major contributor to this trend. Additionally, a new ordering wave of low-speed, “eco” bulkers was encouraged by Chinese government spending, as well as attractive yard pricing. The slower growth rate of the fleet in engine power terms has also been influenced by ‘upsizing’, in containerships in particular. Boxships are now being delivered with capacities of more than 20,000 TEU. These have lower power/TEU ratios. This means they start to contribute less to kW additions, and indeed to emissions on a per TEU basis.

At the same time, many less power efficient, smaller boxships have been scrapped. In numbers terms, the containership fleet has declined over the last 18 months, such that the total kW output of the containership fleet actually fell across 2016. Overall fleet growth in kW fell to 1.6% in 2016, with oil tankers and gas carriers taking a greater share of net growth. Oil tanker deliveries rose by 68% in GT in 2016, while 23% more gas carrier tonnage was delivered (this led to 4.8% fleet growth in kW for oil tankers, and 9.2% for gas carriers).

No Magic Answers

Overall, since 2009 the fleet’s average main engine power per GT has declined by 10% to 0.43 kW/GT, having previously been steady for more than a decade. Lower power does not automatically mean lower emissions, but the new generation of “eco” ships has been helpful, both for bunker bills and the environment. Of course, this is far from the end of the story: shipping still has a long way to go as part of the future push towards a lower carbon world

https://sin.clarksons.net/features/Details/49844